Partner Evaluation and Reward

Blogs:- Mini, Micro and Maxi …

I hope you find these mini, micro and maxi blogs a stimulating read.

The blogs are a set of hypothesis and insights that I intend to develop into a book and, in a few cases, through academic research into testable theories. They are based on my experiences in the legal industry over the past 30 years.

I will add mini and micro blogs periodically and if you have a particular topic that you would like to see explored, then let me know. If it’s within my compass, I’ll give it a go.

David

July 2020

July 2020

- The Unbalanced Scorecard – Multidimensional Evaluation of Partner Performance

- Why Most Partner Annual Reviews Are a Waste of Time – and what to do about it

July 2020

“The Unbalanced Scorecard”

Multi-dimensional Evaluation of Partner Performance

——————————————–

“Not everything that counts can be counted, and not everything that can be counted counts.”

William Bruce Cameron

Informal Sociology

Developing an “unbalanced scorecard” for use in partner performance evaluation can deliver significant positive business impact by aligning evaluation, and the consequences that flow from it, with delivery of your firm’s key strategic goals and business imperatives.

Financial outputs are used as a proxy for partner performance. Though analysis and action on the basis of financial outputs remain critical tasks for your leadership teams, that analysis can only ever provide a partial and fractured picture of a partner’s overall contribution to the business.

As law firms evolved to become significant businesses, best practice has been to closely monitor the financial outputs achieved by partners, teams and offices. This helped identify areas of financial over and under-performance. Using these financial proxies for performance has been a success and worked very well over the period when most legal services commanded a similar profit and pricing premium and the contribution expectations of each partner were assumed to be roughly similar.

The market environment that confronts the legal industry now, however, is vastly more evolved and volatile. Sometimes described as a VUCA environment, for ambitious firms, this necessitates a further evolution of how your leadership teams evaluate business performance and allocate performance related elements of profit shares.

Your leadership team will need to go beyond reliance on financial data if it is going to deal effectively and consistently with some key questions (see below) and balance competing needs over the medium to long-term.

- Clients– now demand a much more sophisticated approach to pricing of legal product – one that is aligned with the value, to them, of the services provided. As such, one of your partners in a “non-premium” area of practice might be delivering market leading advice to the firm’s marque client base and deriving the maximum possible levels of profit. Whilst another of your partners, servicing the same client base in a “premium” priced area of practice, might well deliver higher absolute levels of profit to the business without needing to be a market leader or as efficient in maximising the profitability of the work delivered.

What is their true relative worth to your business?

- Competition for Talent – is much hotter, and the market for partner moves has become much more fluid. Top partner talent with proven revenue generation capability is much sought after and highly rewarded – this has led to partnerships routinely losing key partners in a way they’ve rarely experienced before.

How do you prevent or respond to demands for greater profit shares from key revenue generating partners?

- Inter-generational Tensions– the VUCA environment, means younger generations of partners are concerned to ensure that they achieve their “deserved” profit shares at the time when their practices are most buoyant. They will move between firms to achieve this end. This has helped drive many firms towards increasing the proportion of performance related profit sharing on offer in their businesses.

How do you ensure enhanced performance related profit shares go to the right partners at the right times?

So, what should your leadership team be doing?

Firstly they should not be throwing the “financial baby” out with the “broader contribution” bathwater! Financial outputs are critical. What I advocate is that your leadership team continues to treat these as the prime measures of partner contribution – but – they should also place an explicit, though less heavily weighted, value on the broader range of contributions each partner makes to the business.

The weighting for each area of expected contribution will vary by firm. How you might decide on and allocate the weightings is worthy of a microblog in its own right. Suffice to say, the weightings should support and reinforce the positive elements of your culture, your strategic goals and business imperatives. Typically, as with my clients, I’d expect the vast majority of firms to allocate at least two thirds of weighted value to partners’ performance in the areas of delivering client service and revenue/profit generation from existing and new clients.

Secondly, you will need to be very specific about the what falls within the bucket of “broader contribution” and how you will measure those contributions – including the metrics you will use.

Ensuring broader contributions are specified, evaluated and given an explicit weighted value delivers at least three highly beneficial outputs.

- Partners who generate significant levels of profitable revenue for themselves and others whilst making strong contributions to the broader business will stand out and be deservedly at the top of performance related profit allocation ladder.

- High revenue/profit generating partners, who otherwise make little or no contribution to the broader business or other partners’ practices, can be distinguished from and rewarded differently to those in 1. above.

- The broader contribution of partners who struggle to perform against the firm’s key financial metrics will become obvious, well defined and valued. This enables your leadership team to make informed decisions as to reward levels and status. Somewhat counter-intuitively, allocating explicit value to specific broader contributions prevents them masking otherwise poor performance, as all partners will be assessed on their broader contribution and not just those who have a poor financial performance record.

Thirdly, to be effective, the explicit value allocated to broader contributions must count towards each partner’s evaluation rating and not be seen as something separate to the evaluation of client facing areas nor seen as an optional extra.

Re-calibrating your firm’s evaluation of partner contribution in this way will allow high levels of performance and contribution to be recognised across a range of areas whilst, at the same time, ensuring that generation of significant levels of profitable income remains the key goal of all your partners. Using this approach, a trusted and clear-sighted leadership team, that is committed to taking action on the basis of the unbalanced scorecard, can create significant positive business impact.

July 2020

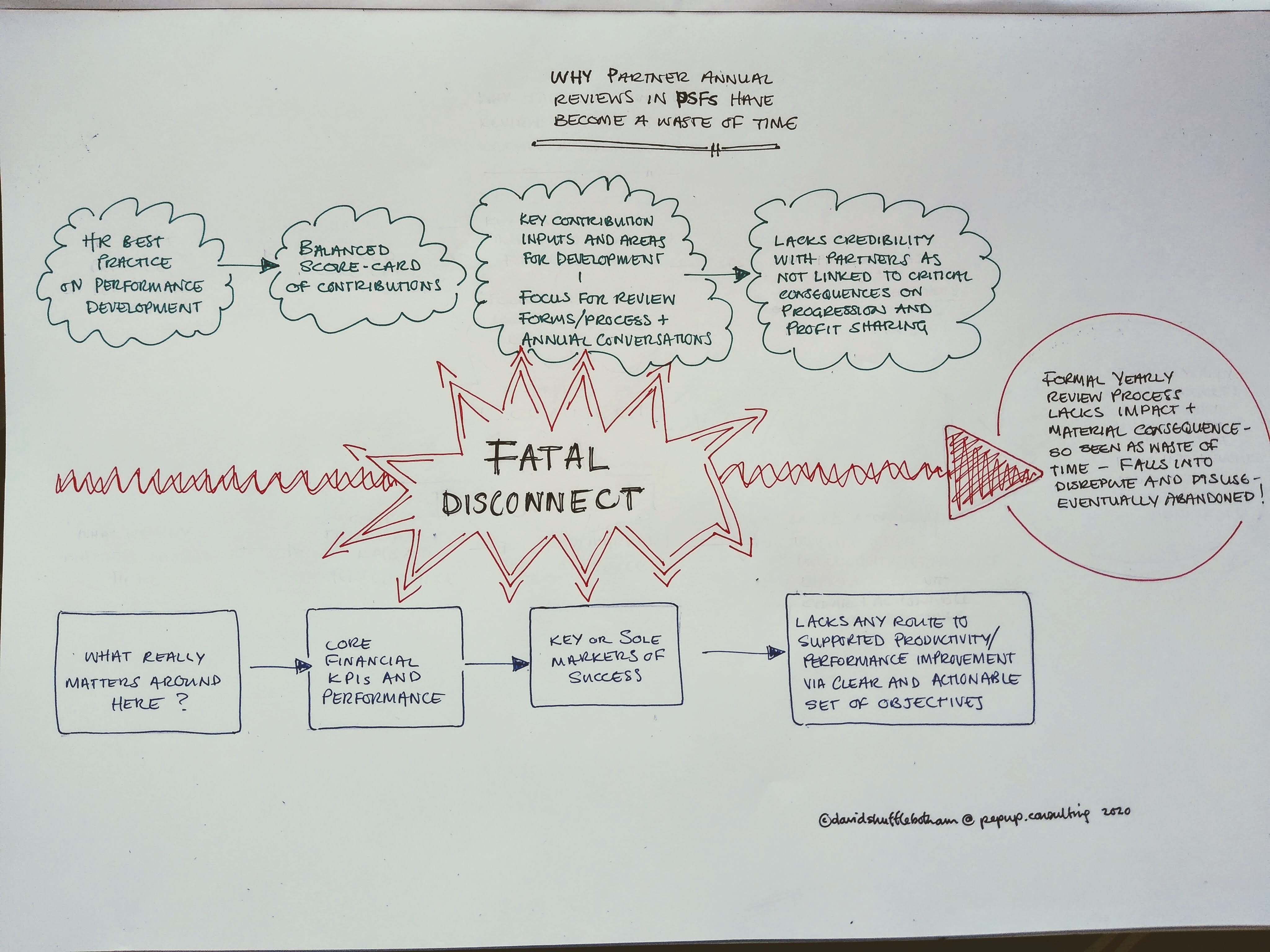

Why Most Partner Annual Reviews Are a Waste of Time

and what to do about it …

——————————————–

BOTH the above approaches have merit in their own right.

BUT, unless integrated, they will confuse and frustrate partners (not to mention everyone else) and lead to much wasted energy and effort. Integrate the approaches and it is possible to generate a consistent and well understood focus on what each partner is charged with delivering.

To integrate the approaches you need your CPOs/HRDs and CFOs/FDs and CMOs/MDs CITO/ITDs etc to be working to the same agenda and to be “literate” in each other’s fields and data sets and systems. This closely collaborative approach will provide your firm with a sound basis from which you can evidence partner contribution to the business, set and support developmental objectives and drive enhanced financial outputs.

Review discussions will have impact and objectives aimed at developing improved plans, actions, attitudes and behaviours can be tracked into the financial outputs the firm is looking to achieve.

April 2021

Partner Compensation – Decision Time

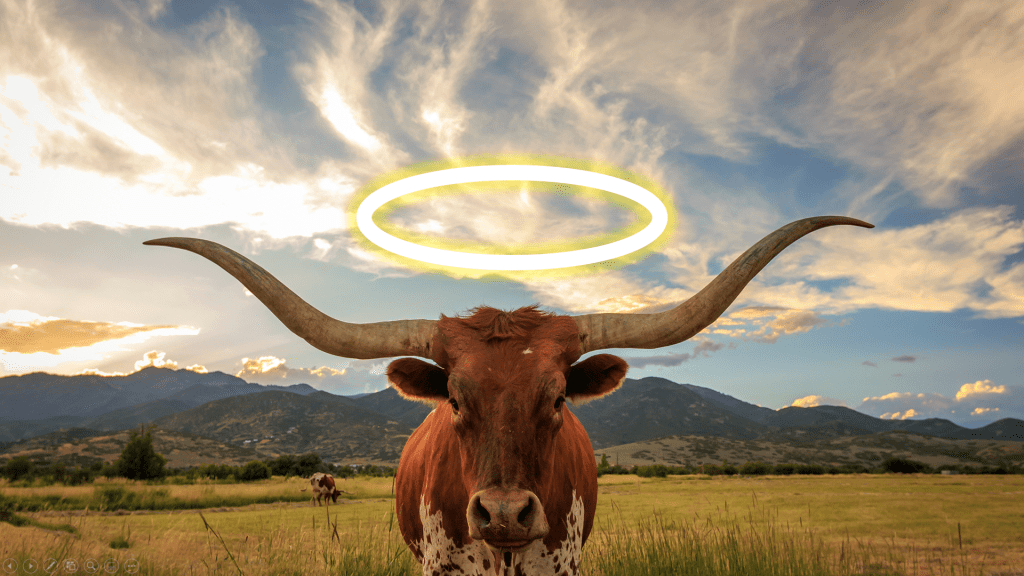

Horns, Halos and “What You See Is All There Is ….“

Are you filled with dread at upcoming partner reviews, reward discussions and decisions? In the first of three short posts designed to help leadership teams improve process and outcomes, I draw inspiration from Daniel Kahneman’s “Thinking Fast and Slow” and give some top tips to assist you in preparing for RemCo deliberations.

Opinions – Beliefs – Intuitions – Decisions

There has been significant market uptake of “unconscious bias” training and resulting development in the thinking around how we form opinions and reach decisions. This thinking is clearly pertinent to the deliberations of your firm’s Remuneration Committee “RemCo”.

Daniel Kahneman in “Thinking Fast and Slow” provides many telling insights in this context but, as you prepare for those RemCo deliberations, these are three to bear in mind:

1. The intuitive parts of our brain help us reach conclusions almost automatically and without having to engage critical thinking faculties. This serves us well if “the conclusions are likely to be correct and the cost of an occasional mistake acceptable”. Intuitive errors are probable Kahneman says when “the situation is unfamiliar, the stakes are high and there is no time to collect more information” also when we are tired and hungry!

2. Our brains will always look to confirm our previously held views and make the current situation conform with them as this provides us with a comforting “emotional coherence”. It also results in us placing metaphorical “horns and halos” on the heads of those we know. They are very difficult to dislodge.

3. Our brains do not naturally reach for information that is not presented to us. What Kahneman christened “What You See Is All There Is”. The brain is very good at creating a coherent story, that confirms our beliefs, from even very limited and poor-quality data. We are not naturally very good at asking – what inputs are we missing that would make this picture more accurate?

THE TIPS

Ensure you are not hungry and that you are well rested.

Give yourselves enough time to deliberate – your decisions will have very significant impact on your key profit generating assets – your people.

Challenge your own and each other’s beliefs and assumptions – be prepared to dislodge those halos and horns.

Consider, in detail, the data at your disposal and get behind it – triangulate the data with other data, information and inputs. There is no single data point that will provide you with a complete answer.

These are critical decisions – slow down your thinking and ask – “what else do we need to know in order to make the best possible decisions?”

May 2021

Partner Reviews and Compensation Decisions

Putting Your Financial Data to Best Use ….

Are you filled with dread at upcoming partner reviews, reward discussions and decisions? In the second of three short posts, designed to help leadership teams improve process and outcomes, I provide some tips on how to put your financial data to best use.

“Essentially, all models are wrong – but some are useful.”

George Box; Norman Draper (1987). Empirical Model-Building & Response Surfaces

Your firm’s financial data is an essential tool for evaluating partner contribution. But you need to take care in how you assess and apply it because your financial data:

- Provides more compelling and comprehensive evidence of contribution in some areas than others.

- Is a proxy for performance, providing an influential but fractured reflection of what a partner actually delivers to the business.

- Can shine so brightly that it blots out all other considerations – how often have you heard – “yes, all that other stuff they do is great – but just look at their numbers!”?

THE TIPS

Consider, for each area of contribution, the extent to which the data is compelling and comprehensive.

Taking client facing activities as our example: the financial data in your practice management system on delivery of legal advice to clients, and getting paid for that work is far more compelling and comprehensive than the financial data available to evidence contribution to client relationship management. So, you can rely with confidence on the data in the former case but will need to look for additional sources of evaluatory input for the latter.

Treat your financial data as a starting point – a useful simplification of reality.

Think closely about what each individual piece of data is actually telling you and confine its influence to that field of contribution. For example, what does “matter partner billing[1]” really provide evidence of, and what doesn’t it evidence.

You should also avoid overly fixating on one measure, especially if that measure is a combination of a number of data sets. I always tell my clients that they will get a more rounded and richer view of partner contributions if they consider a range of “raw” data, rather than an amalgamated single number.

And it is always wise to remember, Charles Goodhart’s adage from 1975 that, “When a measure becomes a target, it ceases to be a good measure.”

Be specific about what falls within your range of expected “broader contributions”.

And ascribe some explicit value to those contributions – maybe 20-30% – and apply it to all partners. Doing this has three key impacts:

- Partners generating significant levels of profitable revenue for themselves and others, whilst making strong broader contributions will, deservedly, come out on top of your evaluatory table.

- High revenue/profit generating partners, who otherwise make little or no broader contribution, will still be highly rated but will not sit at the top of your evaluatory table.

- The broader contribution of partners who struggle to perform against the firm’s key financial metrics will become obvious and have a specific value attached. Once specifically valued, somewhat counter-intuitively, this prevents it excusing below par partner performance against key financial metrics.

January 2022

Partner Reviews and Compensation Decisions

Evaluating “Broader” Contribution ….

In the third and final of three short posts, designed to help leadership teams improve process and outcomes, I provide some tips on how to approach evaluating “broader” partner contributions. Those “hard to measure” contributions that fall outside short-term client service commitments and don’t show up in your financial reporting, but which have a profound effect on long-term and sustained business success.

——————————————————-

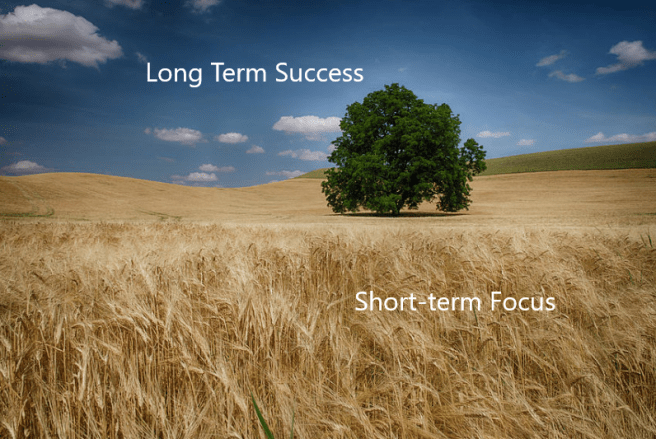

“If we value the present much more than the future, then we’re less likely to make the necessary investments today to reduce risk tomorrow.”

In his 2020 Reith lectures Dr Mark Carney distinguishes between: (1) the short-term focus and commitment to client service and relationships that are critical to a businesses’ current fortunes, and that tend to be the driver of individually focused remuneration models; and (2) the sort of contributions that amount to “investments in long-term business success”.

The Reith Lectures 2020: How We Get What We Value – From Moral to Market Sentiments

——————————————————-

As a leader at your firm, you recognise your partners’ laser-like focus on short-term client service and relationships remain critical to your fortunes. You also agree with Mark Carney that the “broader” contributions they make are fundamental to the sustained long-term success of your business.

But you have a problem. At your firm, in common with many others, “broader” contributions are given little, or no, actual recognition or value when assessing partner performance or setting remuneration. As a result, you struggle to get partners to focus on and deliver these meaningful broader contributions to the extent you’d like them to.

To ensure the sustained and stable success of your firm, you want to change this state of affairs. You want to direct at least some of your partners’ focus towards broader business critical tasks and initiatives, as well as to client service and relationships.

So, here are some tips to help you do just that.

THE TIPS:

Define it – Define what you want partners to contribute in each of these broader contribution areas. Make sure the descriptions support your strategic aims and reinforce positive cultural alignment. For example, by setting out the type of collaborative intent and action you expect partners to demonstrate. Typical areas of broader contribution might encompass: People & Talent , Risk & Ethics, Firm Leadership & Culture, Technical Excellence & Knowledge Sharing.

Get your partners to help you with the definitions – they’re good at this. Ask them to describe what the best partners in a given area do and how they do it. Also ask them what they’d expect a baseline level of partner contribution to look like. Then fill in the gaps.

Value it – As noted in an earlier blog, give an explicit value to each area of broader contribution. This helps indicate where, and to what extent, you expect partners to direct their focus, time and energy and it ensures that contributions in “broader” areas have evaluatory and remuneration consequence. It also means that you are making good on any assertions that your culture ensures that client-facing financials are not the only thing that matters at your firm.

Evidence it – Go looking for, and start to build, a data set that can act as supporting evidence that your partners can use to demonstrate what they have been delivering. The data is out there and it doesn’t take long to identify it – but it’s not just sat in your Practice Management (Financial) System. So go looking in your HR System, Client Contact System, Document and KM Systems, telephone and email records, risk register and management reports. But also ensure the data you use links to the definitions of expected contribution you have put in place (see 1. above) and not just what is easy to collect.

Contextualise it – Take input from your subject matter experts – Chiefs of Finance, HR, BD, IT, KM, Risk. They have a wealth of experience and in depth knowledge of partner behaviours – good and bad. Have them curate, interpret, contextualise and report against the supporting evidence data set you’ve built. But take care to ensure the their input is provided on a structured, well understood and consistent basis, otherwise their input and the data will be easily undermined.